经济学人 | 全球能源市场面临灾难 | Global energy markets are on the verge of a disaster

Scenarios now range from bad to awful

各种情景现在从糟糕到极其糟糕

TRADERS OF OIL futures are a sunny bunch. On April 17th, after Iran’s foreign minister declared the Strait of Hormuz “completely open”, the price of Brent crude fell by 10%, to $90 a barrel. Within hours Iran reversed course and attacked an Indian tanker. The next trading day the global benchmark rose by just 5%. It has gone back up above $100 since but remains around $15 below its high in late March, even though an American blockade has trapped even more oil in the Gulf.

石油期货交易者们是一群阳光的人。4 月 17 日,在伊朗外长宣布霍尔木兹海峡“完全开放”后,布伦特原油价格下跌 10%,至每桶 90 美元。几小时后伊朗改变立场并袭击了一艘印度油轮。下一个交易日,这一全球基准价格仅上涨了 5%。此后它已回升至 100 美元以上,但仍比 3 月下旬的高点低约 15 美元,尽管美国的封锁已将更多石油困在海湾内。

Fifty days into the Iran war the world has lost 550m barrels of Gulf crude—nearly 2% of last year’s global output. Every month Hormuz stays closed, the world misses out on 7m tonnes of liquefied natural gas (LNG), worth 2% of its annual supply. Yet in Western countries, which host the largest futures markets, pain remains limited. Petrol is a bit pricier, but most households can still afford to drive. Trucks keep trucking. Planes continue to fly. Fuel stocks remain close to pre-war levels.

伊朗战争爆发 50 天后,世界已损失了 5.5 亿桶海湾原油——约占去年全球产量的 2%。霍尔木兹海峡每关闭一个月,世界就错失 700 万吨液化天然气(LNG),占其年供应量的 2%。然而在拥有最大期货市场的西方国家,痛苦仍然有限。汽油价格略有上涨,但大多数家庭仍能负担得起开车出行。卡车继续运输。飞机继续飞行。燃料库存仍接近战前水平。

This comforting picture is deeply misleading. By April 20th the last few oil tankers to cross Hormuz before the war began reached their destinations, in Malaysia and California. There is no buffer left to protect the world from the supply shock, at a time of the year when demand from holiday drivers starts to pick up.

这一令人安心的画面极具误导性。截至 4 月 20 日,战争爆发前穿越霍尔木兹海峡的最后几艘油轮已抵达其在马来西亚和加利福尼亚的目的地。再也没有缓冲来保护世界免受供应冲击的影响,而此时度假驾驶者的需求正开始上升。

To gauge how close the world is to energy catastrophe, The Economist has collected a dashboard of indicators. It shows grave harm has already been done. Worse, without a reopening costs could soar, triggering events that cause the fuel system to seize up. A reopening of the strait now would—just—avoid calamity. But some additional pain is already inevitable.

为了评估世界距离能源灾难有多近,《经济学人》整理了一个指标仪表板。它显示严重的损害已经造成。更糟的是,如果不重新开放海峡,成本可能会飙升,触发导致燃料系统瘫痪的事件。现在重新开放海峡——勉强——可以避免灾难。但一些额外的痛苦已经不可避免。

Three factors are pushing the world towards the cliff edge. Oil cargoes available to buy are drying up. Refineries are slashing output of fuel. And demand remains artificially high, especially in Europe. Something big must give somewhere large for energy markets to balance.

三个因素正将世界推向悬崖边缘。可供购买的石油货运正在枯竭。炼油厂正在削减燃料产量。而需求仍然人为地高企,尤其是在欧洲。能源市场要实现平衡,某处必须出现巨大的变化。

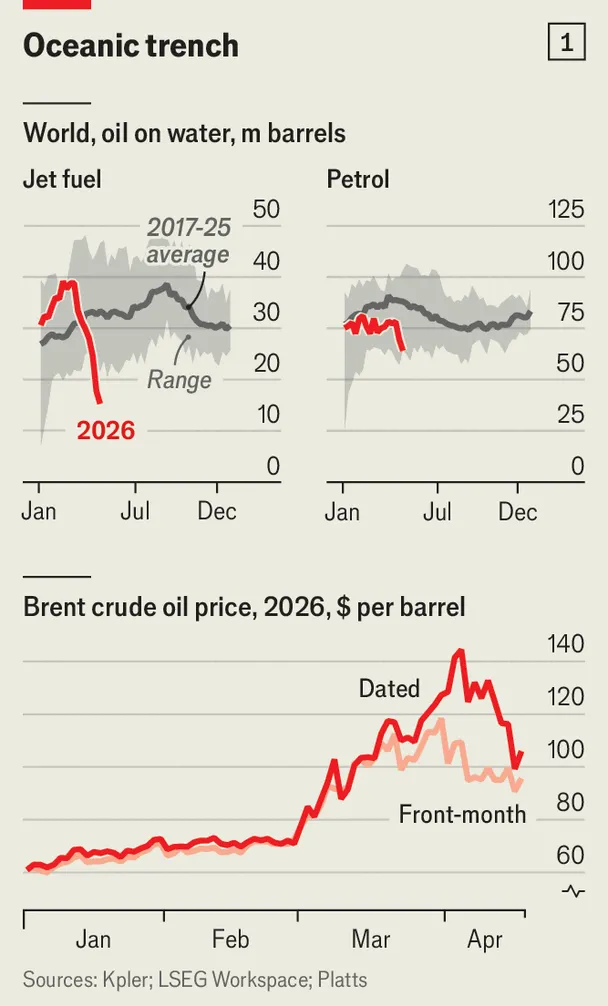

Take trade first. One reason the largest supply shock in petroleum history has not triggered global panic is that a near-record amount of oil was already at sea when the war started. As American warships set sail for the Gulf in February, countries there cranked up exports. After the latest deliveries, those excess seaborne stocks are now exhausted. So are most cargoes of Iranian and Russian oil, which were loitering at sea but found buyers after America eased sanctions on the two countries. Total volumes on water have fallen at record speed. For jet fuel and petrol they are well below historical norms, and possibly close to the minimum required for seaborne trade to function (see chart 1, top panel).

先看贸易方面。石油史上最大的供应冲击之一没有引发全球恐慌的一个原因是,战争爆发时已有接近创纪录数量的石油在海上运输。2 月美国军舰向海湾进发时,各国纷纷加大出口力度。在最近一批货物交付后,那些多余的海上库存现已耗尽。大部分在海上徘徊的伊朗和俄罗斯石油也在美国对两国放宽制裁后找到了买家。水上运输总量以创纪录的速度下降。航空燃油和汽油的运输量远低于历史正常水平,可能已接近海上贸易运作所需的最低限度(见图 1,上图)。

This leaves Asia, which used to receive four-fifths of Gulf exports, in a particular bind. Commercial inventories in a few other Asian countries are running out. South Korea is due to taper releases from its strategic reserves in the coming days. Japan’s will be exhausted in May. Crude stocks in Asia excluding China fell by 67m barrels, or 11%, in the month to April 19th, according to Kayrros, a firm that estimates inventories using satellite imaging.

这使得曾经接收海湾出口量五分之四的亚洲陷入了特别的困境。其他一些亚洲国家的商业库存即将耗尽。韩国将在未来几天逐步释放其战略储备。日本的储备将在 5 月耗尽。据使用卫星成像估算库存的 Kayrros 公司数据,截至 4 月 19 日的一个月内,不包括中国在内的亚洲原油库存下降了 6700 万桶,即 11%。

A shortfall of raw materials has forced Asian refiners to cut throughput by over 3m barrels a day (b/d), or 10% of their combined capacity. That could accelerate to 5m b/d in May and, if the strait stays shut, 10m b/d in July, says Neil Crosby of Sparta Commodities, a data firm. China could help by releasing some of the 1.3bn barrels of crude it holds in reserve. Instead it has suspended exports of refined products. A trader familiar with its energy strategy reckons it will not open the taps before a lasting truce. All this compounds shortages created by the loss of Gulf exports of finished fuel, on which Asia also relies.

原材料短缺迫使亚洲炼油厂削减了超过 300 万桶/日的加工量,即其综合产能的 10%。Sparta Commodities 数据公司的尼尔·克罗斯比估计,这一数字可能在 5 月加速至 500 万桶/日,如果海峡持续关闭,7 月将达到 1000 万桶/日。中国可以通过释放其持有的 13 亿桶原油储备来提供帮助。但它反而暂停了成品油出口。一位熟悉其能源策略的交易员估计,在达成持久停火之前,中国不会开闸放油。所有这些都加剧了亚洲同样依赖的海湾成品油出口损失所造成的短缺。

Refined-fuel prices are already high. In Asian spot markets, petrol nears $120 a barrel, diesel $175 and jet fuel $200, up from $80, $93 and $94, respectively, before the war. Demand is adjusting, partly by government decree. Seven countries have imposed work-from-home mandates and at least five are rationing vehicle fuel. High prices are doing their bit, too. Small miners, fisheries and other firms without adequate diesel stocks are working part-time. Unable to afford naphtha, another oil product, some plastic-makers have shut units. The combination of state and self-imposed rationing may cause Asian crude demand to shrink by nearly 3m b/d in April, compared with February.

成品油价格已经居高不下。在亚洲现货市场上,汽油接近每桶 120 美元,柴油 175 美元,航空燃油 200 美元,分别从战前的 80 美元、93 美元和 94 美元上涨。需求正在调整,部分是通过政府法令。七个国家已实施居家办公令,至少五个国家正在对车辆燃油实行定量配给。高价格也发挥了作用。没有足够柴油库存的小型矿业公司、渔业公司和其他企业正在兼职运营。一些塑料制造商因无法负担另一种石油产品石脑油而关闭了部分装置。国家和自我实施的配给相结合,可能导致 4 月份亚洲原油需求比 2 月份减少近 300 万桶/日。

Europe has so far avoided demand destruction, as governments try to preserve citizens’ purchasing power. Of the 27 European Union countries, 16 are using taxpayer money or cutting fuel taxes to shield consumers from higher prices. European refiners have thus barely slashed production. But, like their Asian counterparts, they, too, must buy crude at a much higher cost than Brent futures suggest.

到目前为止,欧洲避免了需求破坏,因为各国政府试图保护公民的购买力。在 27 个欧盟国家中,有 16 个正在利用纳税人的资金或削减燃油税来保护消费者免受更高价格的影响。因此,欧洲炼油厂几乎没有削减产量。但是,与亚洲同行一样,它们也必须以远高于布伦特期货价格的成本购买原油。

A better gauge is Dated Brent, the price for real cargoes delivered in the next few weeks. The spread between the two—usually $1-2—widened greatly in April, reflecting fears of near-term shortages, according to Platts, which produces the benchmark (see chart 1, bottom panel). It has narrowed since but remains bigger than usual (and does not include eye-watering freight rates and other costs).

一个更好的指标是 Dated Brent,即未来几周内交付的实际货物的价格。据生产该基准价格的普氏能源资讯称,两者之间的价差——通常为 1-2 美元——在 4 月大幅扩大,反映了对近期短缺的担忧(见图 1,下图)。此后价差有所收窄,但仍大于正常水平(且不包括令人咋舌的运费和其他成本)。

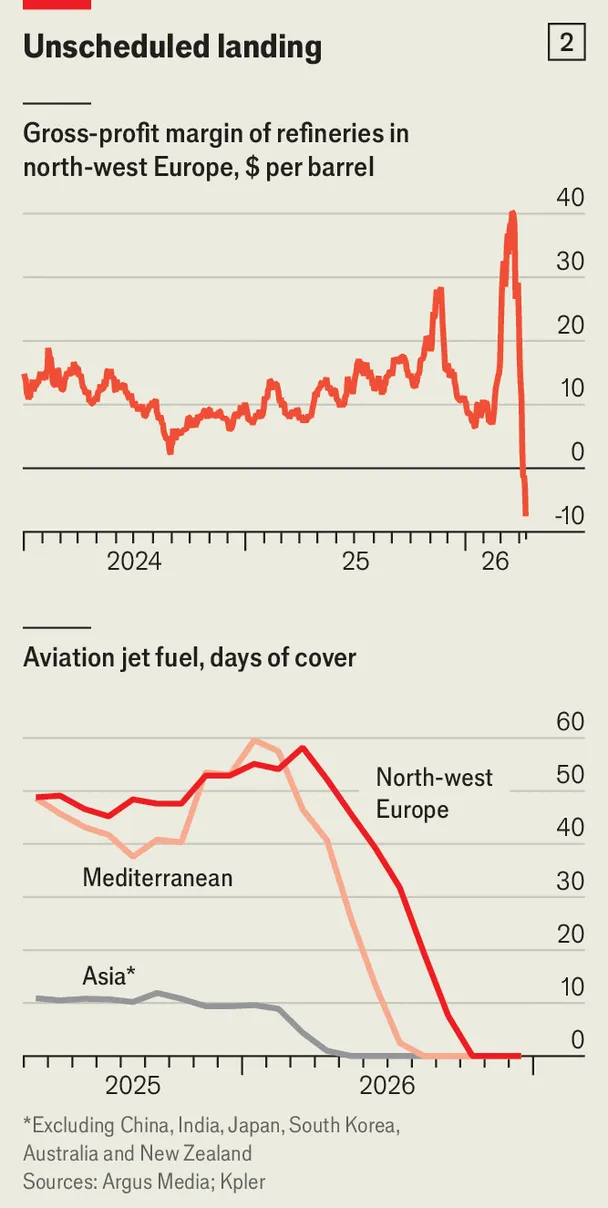

Raw material at $130-150 a barrel has pushed European refiners’ margins into the red, reckons Benedict George of Argus Media, a price-reporting agency (see chart 2, top panel). Extreme backwardation—when commodity spot prices are much higher than those for futures—crush their profits: they must pay up for crude now but sell their products at lower futures prices. Before long they will need to cut output.

价格报告机构 Argus Media 的本尼迪克特·乔治估计,每桶 130-150 美元的原材料已将欧洲炼油厂的利润率推入亏损(见图 2,上图)。极端的现货溢价——即大宗商品现货价格远高于期货价格——压缩了它们的利润:它们现在必须为原油支付高价,但以较低的期货价格出售产品。不久之后,它们将不得不削减产量。

If Europe keeps subsidising consumption, markets will get more out of whack. For one thing, prices for products will keep rising. America, where demand tends to jump in a period of summer road trips, will push them further. Competition for LNG, shortage of which was mostly absorbed by Asian consumers’ self-deprivation and a switch to coal, will also increase when Europe starts restocking gas for the winter.

如果欧洲继续补贴消费,市场将更加失衡。一方面,产品价格将继续上涨。在夏季公路旅行期间需求往往会上升的美国将进一步推高价格。此前 LNG 短缺主要被亚洲消费者的自我克制和转向煤炭所吸收,当欧洲开始为冬季补充天然气储备时,对 LNG 的竞争也将加剧。

Fast-depleting stocks make matters worse. Europe’s reserves of jet fuel cover some 50 days of consumption, their typical level. But modelling by Michelle Brouhard of Kpler, a data firm, for The Economist shows that European stocks will fall precipitously if Hormuz flows do not normalise by June. Those in other importing regions may disappear even faster (see chart 2, bottom panel). The outlook could worsen if America, seeking to tame domestic prices, emulates China and bans exports of refined products, which have risen by nearly half since the start of the war.

快速消耗的库存使情况更加恶化。欧洲的航空燃料储备可维持约 50 天的消费量,处于其典型水平。但数据公司 Kpler 的米歇尔·布罗哈德为《经济学人》进行的建模显示,如果 6 月前霍尔木兹海峡流量不能恢复正常,欧洲的库存将急剧下降。其他进口地区的库存可能消失得更快(见图 2,下图)。如果美国为控制国内价格效仿中国禁止成品油出口(自战争开始以来已上涨近一半),前景可能会更加恶化。

Futures markets are in denial about all this. Even if Hormuz reopened today, it would take months for Gulf crude output, shipping and refining to resume in full. Saad Rahim of Trafigura, a trader, thinks a cumulative loss of 1.5bn Gulf barrels, or 5% of annual global output, is almost unavoidable. If the strait stays closed, it could easily reach double that. The last time oil demand fell by 10% in short order was during the covid-19 lockdowns of 2020, a shock that also brought about a fall in world GDP of more than 3%. The time to avoid a similar tumble is running out. ■

期货市场对所有这一切都视而不见。即使今天霍尔木兹海峡重新开放,海湾原油产量、航运和炼油业也需要数月才能全面恢复。贸易商托克公司的萨阿德·拉希姆认为,累计损失 15 亿桶海湾石油,即全球年产量的 5%,几乎是不可避免的。如果海峡持续关闭,这个数字很容易翻倍。上一次石油需求在短时间内下降 10% 是在 2020 年新冠疫情期间,那次冲击也导致全球 GDP 下降超过 3%。避免类似崩溃的时间正在耗尽。■