2026年4月06日至4月10日 航运市场周报

航运市场综述 (Market Overviews)

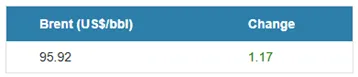

Earlier this week, on 7 April, Donald Trump announced a ceasefire brokered by Pakistan, halting US and Israeli military operations against Iran and securing the reopening of the Strait of Hormuz. Oil prices subsequently fell significantly on 8 April.

本周早些时候,4月7日,唐纳德·特朗普宣布由巴基斯坦斡旋的停火协议,暂停美国和以色列针对伊朗的军事行动,并确保霍尔木兹海峡重新开放。随后,4月8日油价大幅下跌。

Despite the ceasefire, physical normalization is expected to lag, as plants will require time to restart or ramp up production. Additional protocols and insurance approvals are also needed, and potential port congestion may delay the full recovery of cargo flows. Most traders are adopting a wait-and-see approach this week before concluding any deals.

尽管达成停火,实体恢复预计将存在滞后,因为工厂需要时间重启或提升产能。还需要额外的协议和保险审批,港口拥堵的可能性也可能延迟货物流的全面恢复。本周大多数交易商在达成任何交易前都采取观望态度。

Freight rates have been hovering within a range of +/- USD 2–4 per metric ton from last-done levels. Owners are exercising caution before committing vessels to transit the Gulf, pending clearer guidance from relevant P&I clubs. War risk premiums are likely to remain at current levels for now, as discussions continue.

运费率在每公吨较上一次成交价上下浮动2–4美元的范围内。船东在收到相关P&I协会更明确的指导之前,对于派船穿越海湾保持谨慎。由于谈判仍在进行,战争风险保费短期内可能维持在当前水平。

-

北行航线 (North Bound)

Chemicals market remains soft this week, mainly due to limited supply caused by plant turnarounds, force majeure, and reduced production rates due to the lack of feedstock. Palms market have also remained soft due to the lack of demand and cargo pricings.

本周化工市场依然疲软,主要原因是因装置检修、不可抗力以及原料不足导致的供应受限和减产。棕榈油市场也因需求不足和货物定价低迷而持续疲软。

Owners continue to face challenges in securing cargoes amid constrained volumes, with vessels opening prompt and seeking suitable employment to fill positions. Larger parcels of BTX and methanol have been worked ahead, primarily targeting May laycan dates.

船东在货运量受限的情况下继续面临争取货源的挑战,船舶即时空船,寻求合适的雇用以填补档期。较大批量的 BTX 和甲醇已提前成交,主要锁定五月的装运期。

In response to the weaker market, some owners are ballasting to South China/Taiwan region in search of better opportunities, while others have softened freight levels by USD 1–2 to secure employment. The fixing window remains at approximately 1–3 weeks.

由于市场疲软,一些船东正在压载前往华南/台湾地区寻找更好的机会,另一些船东则将运费水平下调 1–2 美元以确保雇用。当前的成交窗口维持在约 1–3 周。

2. 南行至海峡地区 (South Bound to Straits)

Inquiries for blending components such as MTBE, MEAC, and toluene have softened this week, as suppliers and traders monitor demand and cargo prices following the ceasefire.

本周对 MTBE、MEAC 和甲苯等调和组分的询盘有所减弱,因为供应商和交易商在停火后正密切关注需求和货物价格。

MEG and methanol inquiries, which surged last week, have eased due to the short window of opportunity. Caustic soda tenders are still circulating, but owners generally treat these as a last resort unless needed to position for their next employment. Freight levels remain largely in line with last-done numbers, with 10kt parcels from North China to the Straits still being discussed in the high USD 40s range.

上周激增的 MEG 和甲醇询盘因机会窗口较短而有所回落。烧碱招标仍在流通,但船东通常将这些视为最后手段,除非需要为下一航次定位。运费水平基本与最近成交价格持平,从中国北部到海峡的 10,000 吨批量仍在讨论美元 40 高段区间。

Bunker prices dropped mid-week, which may lead to some softening in freight rates, while some traders are waiting to see if the trend continues into next week. The current fixing window stands at approximately 3–4 weeks.

周中燃油价格下跌,可能导致运费率略有走软,一些交易商则在观望这一趋势是否会延续到下周。目前的签约窗口大约为 3-4 周。

3. 远东至印度/阿拉伯湾 (FEA to India/AG)

Market activity remains focused on typical products such as styrene monomer (SM), aromatics, and AA & alcohols, with parcel sizes ranging from 5,000 to 15,000 metric tons, primarily moving from China and Korea to India.

市场活动仍集中在苯乙烯单体(SM)、芳烃以及AA和醇类等常规产品,批量规模在5,000至15,000公吨之间,主要从中国和韩国运往印度。

Methanol inquiries from China to India eased this week, with a 15,000-ton cargo reportedly fixed from South China. Freight is expected in the low $80s/mt.

本周来自中国到印度的甲醇询盘有所放缓,据称南中国有一批15,000吨的货物已成交。运费预计在每公吨80美元出头。

Overall, rates for 10,000–20,000-ton parcels have held in the low $80s/mt over the past two weeks, with owners continuing to ask for a premium due to the scarcity of backhaul cargoes out of India and the Middle East. The fixing window currently remains around 3 weeks.

总体而言,过去两周10,000至20,000吨批量的费率保持在每公吨80美元出头,船东因印度和中东回程货源稀缺而持续要求溢价。当前固定窗口约为3周。

4. 阿拉伯湾/印度西海岸 (AG/WCI)

Despite the ceasefire allowing vessels to transit through the Strait of Hormuz, cargo inquiries have yet to pick up, as plants require time to ramp up production and owners await guidance from P&I clubs before handling cargoes in and out of the Gulf.

尽管停火协议允许船只通过霍尔木兹海峡,但货运询盘尚未回暖,因为工厂需要时间提升产量,船东也在等待保赔协会的指导意见,以便处理进出海湾的货物。

Requirements for the Fujairah-to-Oman range have remained relatively stable, while owners continue to monitor developments from the relevant P&I clubs regarding war risk premiums.

富查伊拉至阿曼航线的需求保持相对稳定,船东继续关注相关保赔协会关于战争风险保费的动态。

Current freight rates are holding at last-done levels, with market participants observing how activity unfolds following the ceasefire. The fixing window is around 2–3 weeks.

目前运费率维持在最近成交水平,市场参与者正观察停火后的活动进展。租船确定窗口约为2至3周。

5. 远东区域内 (Intra–Far East Asia)

COA volumes have remained soft this week, with only a few small parcels quoted in the spot market for chemicals such as acetic acid, methyl acetate, and butyl acetate from China to Korea for end-April to 1H May loading.

本周 COA 运量持续疲软,仅有少量化学品(如醋酸、醋酸甲酯、醋酸丁酯)从中国运往韩国的现货报价,装载时间为 4 月底至 5 月上旬。

This underperformance in COA volumes is largely attributed to ongoing plant turnarounds in Korea, while other producers have scaled down production rates. These cargoes are mostly still in the working stage, facing challenges in conclusion due to pricing gaps between charterers and owners.

这一 COA 运量表现不佳,主要归因于韩国持续的工厂检修,同时其他生产商也降低了生产速率。这些货物大多仍处于洽谈阶段,因租船方与船东之间的价格差距而难以成交。

The tonnage list remains relatively long amid limited spot cargoes and weaker COA liftings. Freight rates have largely held at last-done levels, with the fixing window currently around 2–3 weeks.

在有限的现货货物和疲软的 COA 装运情况下,船舶运力名单仍相对较长。运价基本维持在最近成交水平,当前签约窗口约为 2–3 周。

6. 东南亚区域内 (Intra–Southeast Asia)

The spot market remains soft compared with last week, apart from some activity in MTBE, pygas, and palm cargoes.

与上周相比,现货市场依旧疲软,除甲基叔丁基醚(MTBE)、裂解汽油(pygas)和棕榈货物的一些活动外。

COA volumes continue to be low and moving slowly, leaving pockets of available space, and in cases of delayed shipments, replacement tonnage can be sourced without difficulty.

COA(合同运输量)成交量持续偏低且进度缓慢,导致局部存在可用空间,在装运延迟的情况下,替代船舶可轻松获得。

Owners remain flexible on forward laycans and can reshuffle positions if earlier requirements arise. Freight levels are largely holding at last-done numbers, with 50kb cross-harbor Singapore rates around USD 105k lumpsum. The fixing window currently stands at 1–2 weeks.

船东在远期装卸期方面保持灵活,如有提前需求可调整船位。运费水平基本维持在前一成交价,跨港新加坡 5 万桶运输费约为 10.5 万美元包干。目前的成交窗口为 1–2 周。

新闻速递 (News Bites)

Asian petrochemical markets are facing increasing disruption following supply shocks linked to Middle East energy flows, leading to tightening availability of key feedstocks such as naphtha, LPG, and aromatics.

亚洲石化市场正面临日益加剧的扰动,原因是与中东能源流动相关的供应冲击,导致包括石脑油、液化石油气(LPG)和芳烃等关键原料的供应趋紧。

This has in turn impacted downstream chains including PX, PTA, MEG, and various solvent-grade chemicals, with supply constraints and logistical disruptions supporting a firming price environment.

这进一步影响了下游产业链,包括对二甲苯(PX)、精对苯二甲酸(PTA)、乙二醇(MEG)以及多种溶剂级化学品的生产,供应限制和物流中断支撑了价格坚挺的环境。

Notably, PTA markets have seen significant upside, with spot prices rising by over 30% cumulatively since the onset of the US–Iran conflict, driven by higher feedstock costs and tightening availability.

值得注意的是,PTA市场出现了显著上涨,自美伊冲突爆发以来,现货价格累计上涨超过30%,主要受原料成本上升和供应紧张推动。

China, which accounts for roughly three-quarters of global PTA capacity, is also facing operational constraints, with around 15% of domestic capacity affected by shutdowns and production cutbacks—equivalent to approximately 11% of global PTA supply being exposed to volatility.

中国作为全球PTA产能的约四分之三,也面临运营压力,国内约15%的产能因停产或减产受到影响,相当于全球约11%的PTA供应面临波动风险。

The knock-on impact is becoming increasingly evident across downstream sectors, particularly in textiles and packaging, where several producers have reduced or suspended operations due to shortages of polyester feedstocks and related intermediates.

这种连锁反应在下游行业中日益明显,特别是纺织和包装领域,由于聚酯原料及相关中间体短缺,多家生产商已减少或暂停生产。

Overall, the situation underscores the region’s strong dependence on stable upstream supply, with ongoing disruptions expected to weigh on production rates, trade flows, and market sentiment in the near term.

总体而言,这一形势凸显了该地区对稳定上游供应的高度依赖,持续的扰动预计将在短期内拖累产量、贸易流动及市场情绪。

The global petrochemical market outlook for 2026 has been significantly disrupted by the Iran conflict, overturning earlier expectations of a supply overhang.

2026年全球石化市场的前景已因伊朗冲突而遭受显著冲击,这推翻了先前对供应过剩的预期。

Ongoing attacks on energy and chemical infrastructure, coupled with shipping disruptions in the Persian Gulf, have curtailed production across the Middle East and parts of Asia, removing incremental supply from the market.

对能源及化工基础设施的持续攻击,加之波斯湾地区的航运中断,已导致中东及部分亚洲地区生产活动受限,从而减少了市场供应增量。

As a result, the industry is shifting from a surplus environment to one of tightening availability, with rising risks of product shortages and upward pressure on prices across key chemical chains.

由此,行业正从供应过剩状态转向供应趋紧的局面,产品短缺风险上升,关键化工链条上的价格面临上行压力。

Supply losses continue to mount amid constrained logistics, further exacerbating imbalances in global trade flows. Even in the event of a near-term resolution, normalization is expected to be prolonged, with recovery in petrochemical production and supply chains likely to extend through the remainder of 2026.

在物流受限的背景下,供应损失持续累积,进一步加剧了全球贸易流动的失衡。即便冲突在近期得到解决,正常化过程预计也将持续较长时日,石化生产及供应链的复苏很可能将延续至 2026 年剩余时间。

Daily Price update as of 09 April 2026

新闻来源:沛君航运

每日航运咨询

扫描下方二维码关注

沛君航运

沛君航运经纪(上海)有限公司

上海市浦东新区滨江大道999号高维大厦4C室

Tel: 86-21-3392 6588

Email: general@peijunmarine.com(General)

评论