摩根大通——如何看待市场波动性

When the market is volatile, it’s natural to want to act on emotion. Here’s how to make sure the decisions are as rational and well-informed as possible.

当市场波动时,想凭情绪行动是很自然的。以下是确保决策尽可能理性且充分信息的教训。

When the market is volatile, some investors get nervous, some want out and others reflexively rush to “buy the dip” and be “opportunistic.” Whatever your feeling about volatility may be, here’s how to make sure the decisions nudged by that feeling are as rational, well-informed, fundamentally sound and supportive of your goals as possible.当市场波动时,一些投资者会紧张,有些想要退出,另一些则本能地急于“买入下跌”并“机会主义”。无论你对波动性有什么看法,以下是如何确保被这种情绪推动的决策尽可能理性、信息充分、基本稳健且支持你的目标。

Normalize the pain让疼痛变得正常化

This hurts. Seeing our account balances, the numbers in our ledger and the lines on the charts swinging up and down is an uncomfortable feeling. Let’s acknowledge that. It’s normal to not like this. No one likes it. Not even those investors who claim to have “high risk tolerance” will find times like this to be without worry. It’s one thing to say you don’t mind a bumpy road; it’s another to be bouncing around in your seat.这很痛。看到我们的账户余额、账本上的数字以及图表上波动的线条,感觉很不舒服。让我们承认这一点。不喜欢这种感觉很正常。没人喜欢。即使是那些自称“高风险承受能力”的投资者,也不会觉得在这种情况下毫无顾虑。说你不介意颠簸的路是一回事;坐在座位上跳来跳去则是另一回事。

It’s okay to not like what we’re going through.不喜欢我们正在经历的事情是可以的。

Ask yourself why问问自己为什么

What worries you? What are your specific concerns and fears about this volatility? Without passing judgement on yourself, take a moment to articulate why volatility is so uncomfortable for you. Are you worried about your discretionary spending, your retirement, your legacy or your multigenerational wealth? Do you fear losing control? For how long, to what end, and with what impact? Be specific.你担心什么?您对这种波动性具体有哪些担忧和担忧?不要对自己评判,花点时间表达为什么波动性让你如此不舒服。你担心的是你的非支配消费、退休金、遗产还是多代财富?你害怕失控吗?持续多久,目的如何,影响如何?具体点。

Naming our concern, saying it out loud, can be a big step toward addressing it and taking away some of the power it holds over our rational thinking.把我们的担忧说出来,是迈出解决问题的重要一步,也削弱它对我们理性思维的影响力。

Embrace perspective and advice 拥抱视角和建议

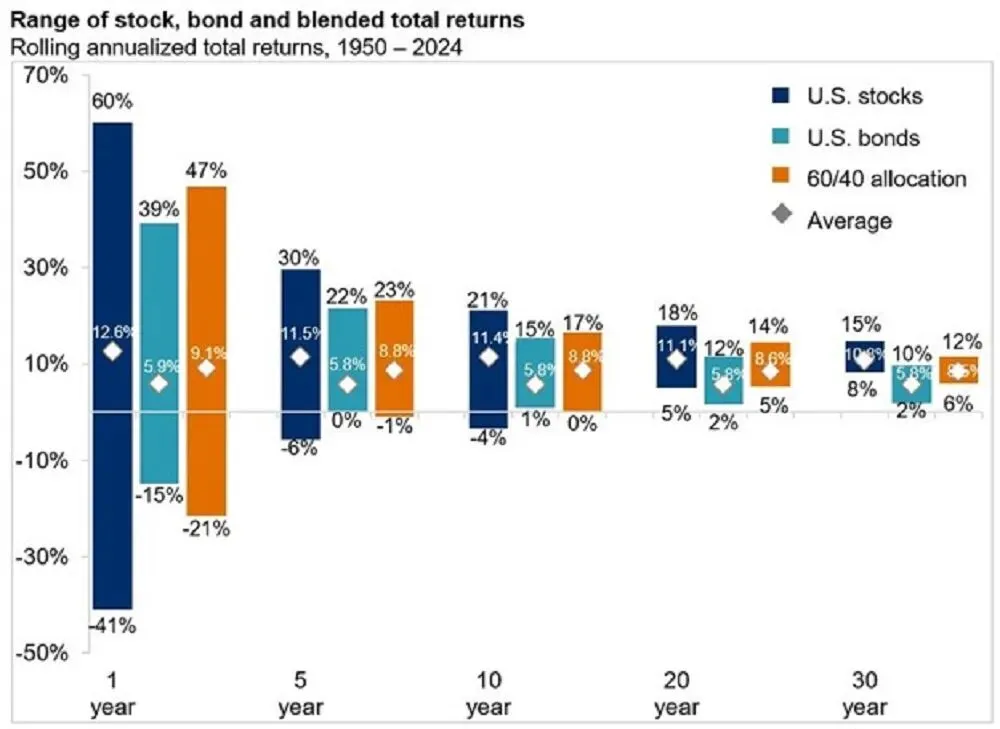

This is part of the process. Market swings are a normal part of the wealth-building process. A painful but normal one. More importantly, volatility is a part of the process for which we plan. You can see how these swings have occurred regularly over the last 40 years in the chart below.这是过程的一部分。 市场波动是财富积累过程中的正常现象。痛苦但正常的。更重要的是,波动性是我们规划过程中的一部分。你可以在下方图表中看到这些波动在过去 40 年中是如何定期发生的。

Despite such swings, markets and investments have gone up over that time, with significant wealth generation along the way. It’s never been an easy, smooth ride upward. It’s always been bumpy. We might think of volatility as the price of admission for a ride that has otherwise rewarded us very well.尽管如此,市场和投资在这段时间内有所上升,并带来了显著的财富创造。这从来都不是一路轻松、平稳的上升之路。一直都很坎坷。我们可能会把波动性看作是一次本来回报丰厚的经历的入场券。

Check your buckets检查你的“资金池”

Mental accounting is the process by which we value money differently depending on the source or use of that money. This may not be entirely rational, but it's quite useful, especially when embracing a goals-based wealth strategy. It allows us to make decisions in one mental account – philanthropy, entrepreneurship, risk-taking – without worrying that it will impact the account or “bucket” where we keep safe the resources that ensure security for our family for decades to come.

心理账户是我们根据资金来源或用途,对金钱赋予不同价值的一种心理机制。这种做法或许不完全理性,却非常实用,尤其是在采用“基于目标的财富管理策略”时。它能让我们在处理某一类账户——无论是慈善捐赠、创业投资还是高风险配置——时,无需担心这会波及另一个专门用来保障家庭未来几十年安稳生活的“安全账户”或“资金池”。

Unfortunately, during times of increased volatility, all our mental accounts can blur together, and it can feel like a risk that only affects one account – our short-term balances, for instance – is affecting all of them. It’s not. There’s more turbulence, but how much of your wealth strategy is dependent upon next year?不幸的是,在波动加剧时期,我们所有的心理账户可能会变得模糊,感觉只影响一个账户的风险——比如我们的短期余额——却影响了所有人。其实不是。虽然动荡会更多,但你的财富策略有多少取决于明年?

Do you think the market will be higher in 10 years than it is today? If so, then let’s separate the wealth accounts that are 10 years out from our decisions based upon today.你认为十年后市场会比现在更高吗?如果是这样,那么我们就把基于今天的决策分开十年后的财富账户。

Volatility risk is mostly about investments tied to the near term, so let’s limit our emotions, reactions and decisions to investment goals in that near term, too.波动率风险主要涉及与短期相关的投资,所以让我们也应将情绪、反应和决策限制在短期内的投资目标。

Sail past present bias驶过现时偏向

The raw emotions of the present are much more tangible and powerful than the distant emotions of an uncertain future. We’re more likely to take action that hurts our future if it feels good right now. In times of volatility, we might do something to reduce the anxiety of the moment even if it harms our long-term outcomes. We might also rush to invest more if we think we’re being opportunistic and “buy the dip” without studying the fundamentals. These are the dangers of “present bias.”

当下的原始情绪远比遥远而不确定的未来情绪更具体、更强大。如果一件事当下让人感觉良好,我们更可能采取损害未来利益的行为。在市场波动时期,我们可能会为了缓解当下的焦虑而采取行动,即使这会损害长期结果。我们也可能在没有研究基本面情况下,就匆忙增加投资,自以为是抓住了“抄底”的机会。这些都是“现时偏向”带来的危险。

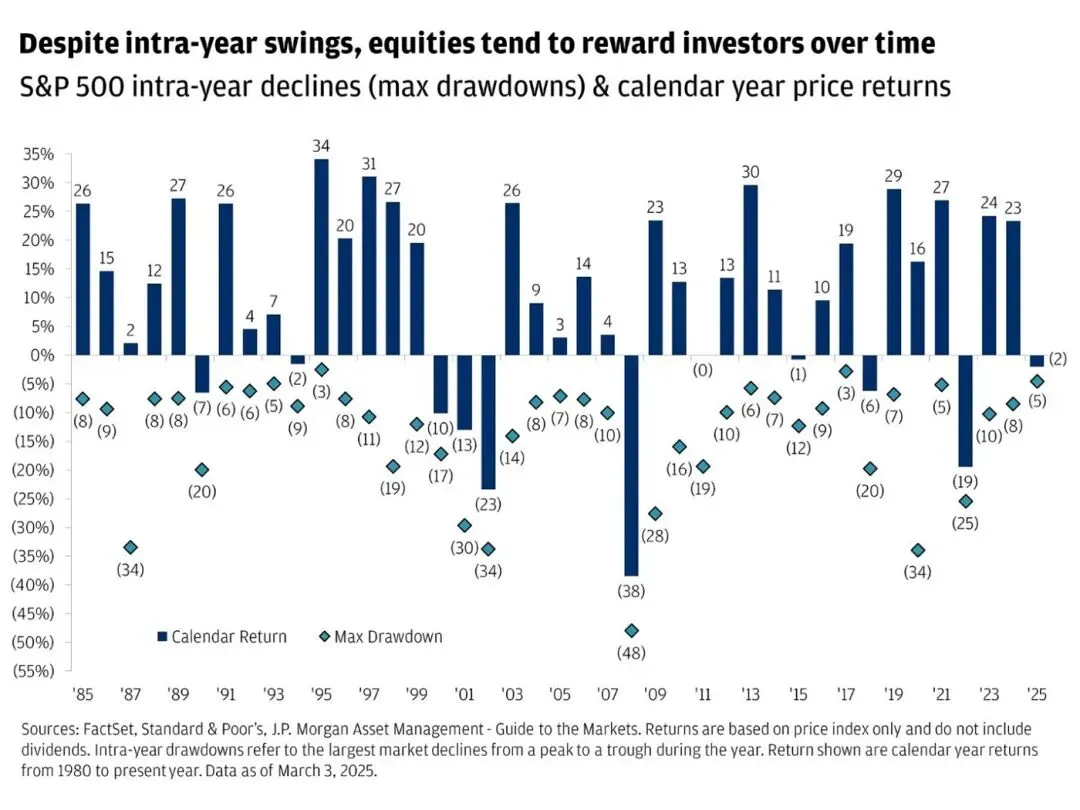

Imagine we’re on a ship in rough water. If we stare at the hull as the waves crash into it, we get seasick. But if we lift our eyes to focus on the horizon, we’ll calm our stomach and be more likely to reach our destination. We should similarly shift our gaze during volatility. Don’t just think about the next six months or a year. Think about the next six years or decade … and beyond. See the chart below.想象我们在一艘船上,水面很糟。如果我们盯着船体看,看着海浪拍打它,我们会晕船。但如果我们抬头专注于地平线,胃部会平静下来 , 更有可能到达目的地。在波动时,我们也应当调整视角。不要只想着接下来的六个月或一年。想想接下来的六年或十年......甚至更远。请参见下方图表。

As our investment horizon expands, volatility shrinks. How will your decisions now impact those goals? That’s what really matters, more than the rough waters of the moment.随着投资视野的扩大,波动性会减弱。你的决定将如何影响这些目标?这才是真正重要的,比当下的波涛汹涌更重要。

The cost of avoiding loss 避免损失的成本

We are more motivated to avoid loss than to pursue gain. We express such loss aversion when we say things like “I don’t want to risk my money” or “I’m worried about getting wiped out.” We do something with our money simply because we’re afraid of losing it.我们更倾向于避免失去,而不是追求收益。当我们说“我不想冒钱风险”或“我担心被彻底毁灭”这样的话时,我们表达了极度的损失恐惧。我们花钱做事,仅仅是因为害怕失去它。

When we pull our money from long-term investments, we may treat that fear of immediate loss, but we lose something else. We lose ground in the pursuit of our financial goals. We lose future lifestyle spending, lose wealth to pass on to the next generation or lose resources to donate to causes dear to us.当我们从长期投资中提取资金时,我们可能会担心立即损失,但我们会失去别的东西。我们在追求财务目标的过程中会失去优势。我们失去未来的生活方式消费,失去传给下一代的财富,或失去捐赠支持我们关心的事业的资源。

There is a tradeoff in every decision.每个决定都有权衡。

If we’ve developed a plan to help reach particular long-term goals – a child’s wedding, a safari, home renovations, retirement – not using all our resources to pursue those goals creates the potential for loss. These long-term losses aren’t just numbers, they’re flower arrangements, extra days in Africa or a pool for the grandkids. They’re the details of our dreams.如果我们制定了帮助实现特定长期目标的计划——比如孩子的婚礼、狩猎旅行、房屋装修、退休——那么没有用尽所有资源去追求这些目标,就有可能带来损失。这些长期的损失不仅仅是数字,更是花卉布置、非洲多待几天或孙辈的游泳池。它们是我们梦想中的细节。

You’re in control你掌控一切

When things are volatile and uncertain – in the markets, in politics, in our family and personal lives – it feels like we’ve lost control. The need for control is powerful. We often take action just to feel like we’re in control. We do something just so that we can Do Something!! It’s natural, and financial action can have noticeable, measurable outcomes, unlike those in politics or family.当局势动荡不确定——无论是市场、政治、家庭还是个人生活——我们都会觉得自己失去了控制。对控制的需求非常强烈。我们常常采取行动,只是为了感觉自己掌控一切。我们做某件事,只是为了能做点什么!!这是自然的,金融行动可以带来明显且可衡量的结果,这与政治或家庭中的行为不同。

Unfortunately, doing something just to Do Something can have consequences for our long-term goals. It may feel like we’re taking control, but when we fail to maximize our resources or undermine our wealth strategy, we’re actually giving up control.不幸的是,仅仅为了做点什么而做某件事,可能会对我们的长期目标产生影响。你可能觉得我们在掌控一切,但当我们未能最大化资源或破坏财富战略时,实际上是在放弃控制权。

Using money wisely is the best way to control our financial future. That’s why we build financial plans and wealth strategies in the first place. And the wealth strategy you’ve built has been structured to anticipate this volatility. We’ve seen the charts, too. You’re in a better position to handle this moment than most because you’ve done the smart, competent, and powerful work of building an informed and thoughtful wealth strategy.明智地使用金钱是掌控我们财务未来的最佳方式。这就是为什么我们最初制定财务计划和财富策略。 而你们构建的财富战略就是针对这种波动性进行设计的。 我们也看过排行榜。你比大多数人更有能力应对此刻,因为你已经做了聪明、有能力且有力的工作,建立了一个有见地且深思熟虑的财富策略。

You are in control. It’s time to show it by making sound decisions with advice tied to your intentions and goals.你掌控一切。现在是时候通过做出与你的意图和目标相关的明智决策来证明这一点。

大家都在看:

国投证券(香港)——以OpenClaw为代表的Agents相关投资机遇分析

国泰海通证券——奇点来临,AI分身加速驱动并放大人类的价值实现

国信证券——人工智能行业深度分析:全球模型巨头的发展路径与商业前景

东吴证券——新债务周期下全球资产重估:“AI-资源-军工”生存三位一体

开源证券——对伊朗经济、石油、贸易与资产价格波动的四个关键观察

华泰证券——太空光伏:从地面领先迈向太空引领的战略性新兴产业

中国银河证券——2026年春节消费解析:消费温和复苏与悦己型消费

国联民生证券——隔热材料:商业航天可回收时代的核心命脉与耗材新蓝海

国联民生证券——北京太空算力:中国天算的“DeepSeek”时刻

开源证券——AI算力基础设施演进:超节点架构的全面解析与产业影响

申万宏源——日本经济全景分析(1945-2024):从复兴到通缩突围的启示

免责声明:本文仅为投资知识分享,不构成任何投资建议。文中提及个股仅为举例说明,并非推荐。市场有风险,投资需谨慎。

评论